At the leadership table, Supply Chain Finance programs are discussed in familiar terms: working capital, supplier stability, channel momentum—and the confidence that key partners won’t slow down because liquidity didn’t arrive on time.

What’s changed is the reality of running these programs at scale. The first phase is often clean: a defined cohort, clear rules, predictable scenarios. The real test begins later, when volumes rise, partner profiles diversify, and the program starts touching multiple teams. That’s when time gets consumed in places no one planned for: invoice confirmation delays, exceptions that bounce between functions, onboarding that stalls, MIS that doesn’t answer review-room questions, and manual workarounds that quietly become “the process.”

By 2026, the shift is in the platform layer behind Supply Chain Finance programs. Better workflows, stronger data trails, and practical AI support are making it easier to expand across suppliers, dealers/distributors, and invoice-led use cases—while keeping control and visibility intact.

This article is a 2026 checklist for Indian corporates: how to design Supply Chain Finance programs that scale smoothly. It also covers what to evaluate in an SCF platform partner, especially if you’re looking to scale without expanding operational load in the same proportion.

Supply Chain Finance in 2026: what’s different for Indian corporates

Most corporate SCF conversations still revolve around familiar levers such as payment terms, liquidity access, supplier stability, and channel momentum. What’s different in 2026 is how efficiently you can run the program when the operating layer is designed well.

Three shifts matter from a corporate point of view:

- More structured invoice trails: as invoicing becomes more standardized and time-bound for many businesses, programs can rely less on manual reconciliation and more on consistent data capture and confirmation steps.

- Better “trust infrastructure”: consent-led data sharing is increasingly mainstream, which can reduce unknowns and speed up verification where counterparties opt in, especially helpful when you move beyond a small, known cohort.

- Practical AI support: the most useful applications are quiet – flagging anomalies earlier, reducing repetitive checks, and improving exception routing, so teams spend time on decisions and partner coordination, not chasing and stitching.

Alongside these shifts, expectations inside the corporate are changing. Top management increasingly wants SCF visibility in the same way they expect visibility in procurement and sales: not a one-off report, but a reliable view of throughput, exceptions, and impact, especially when SCF spans multiple partner types and more than one program model.

The checklist below is designed to help you lock the decisions that matter before you scale.

The 2026 checklist for Supply Chain Finance programs

1. Outcome clarity

Identify the primary outcome of the program in one sentence – what must improve for the business. Keep it in business terms, not product labels. Typical outcomes include supplier stability, procurement continuity, receivables predictability, or channel momentum. Then define 2–3 measures that leadership will review consistently. A practical mix is: (a) coverage (how much of the relevant partner universe is active), (b) utilization and cycle time (how quickly funds move from confirmation to settlement), and (c) exception load (how much effort is consumed by mismatches, disputes, and reversals).

If you’re choosing between two outcomes, choose the one that is most time-sensitive for the business. Programs become easier to run when the operating model is optimized for one primary outcome and supported by one secondary outcome, not stretched across four.

2. Perimeter and sequencing

Decide where you will scale first and how you will expand. A deliberate perimeter reduces ambiguity across teams and keeps the program teachable.

Lock (a) the first business unit / geography / category, (b) the first counterparty cohort, and (c) the expansion sequence—pilot cohort → wider tier → additional geographies/categories → next use case. Avoid expanding cohorts and adding new use cases at the same time; it makes root-cause analysis harder when friction appears.

Also decide what “good participation” looks like for the first perimeter. A pilot that onboards many counterparties but has low repeat usage is telling you something about friction, not demand.

3. Program mix

Most corporates ultimately run more than one program type because suppliers, procurement, channel partners, and receivables behave differently. Choose the mix by mapping partner type to cash-flow constraint and operating reality.

Keep the decision principle simple: don’t force one structure to solve multiple cash-flow problems. If you need supplier stability and channel momentum, treat them as distinct tracks with shared governance and MIS, not as one stretched process.

As you add program types, keep one backbone: the same definition of confirmation, the same exception handling logic, and one reporting layer. That’s what keeps scale manageable when the program mix evolves.

4. Governance that resolves decisions fast

Set one accountable program owner (typically Treasury or Finance Ops) and name owners for three routines that determine program quality: partner onboarding and support, confirmations and exception resolution, and MIS plus review cadence. Define a clear “final call” route for conflicts (for example, sales vs finance on confirmation timing, procurement vs finance on eligibility).

Finally, align incentives early. If sales teams are measured purely on volume and procurement teams purely on cost, they will optimize for their own outcomes unless the program explicitly rewards clean behavior – timely confirmations, fewer disputes, and predictable closure.

5. The invoice truth

Define what triggers eligibility and what “confirmed” means. This is the single most important operational decision in the program.

Be explicit on: the confirmation event (acceptance/GRN/service sign-off/etc.), who is authorized to confirm, what evidence is required, and what happens when confirmation doesn’t arrive within the expected window.

A useful practice is to define a “default path” and an “exception path.” The default path should be fast and repeatable. The exception path should be structured and time-bound, so it doesn’t become a backlog that quietly grows with volume.

6. Exception design

Treat exceptions as normal operations. At scale, returns, credit notes, partial deliveries, and mismatches are not edge cases – they are recurring patterns.

Define standard exception categories, owners, and timelines. Decide how adjustments are handled (credit notes, reversals, short payments), how stale items are closed or re-routed, and how master data changes (GST/bank/entity updates) are verified without restarting the entire onboarding flow.

Also decide how you will handle repeated exceptions. If the same cohort or business unit generates the same mismatch week after week, the solution is rarely “more follow-up.” It is usually a tighter definition, a cleaner data field, or a clearer confirmation step.

7. Controls that scale with partner tiers

Controls should protect speed and discipline together. Segment controls by partner tier so you apply the right depth where it matters.

High-volume or higher-risk cohorts can carry tighter limits and stronger evidence requirements. Mid-tier cohorts can run on standard controls with periodic review. Long-tail cohorts should have simplified rules with smaller limits and clear triggers.

Regardless of tier, core integrity checks (duplication, mismatch, confirmation validity) should be consistent—because consistency is what keeps governance credible. The best controls are the ones that are predictable and invisible during a normal cycle, but extremely clear during a review.

8. MIS built for steering, not reporting

MIS should answer review-room questions quickly: where the program is active, what’s growing, what’s stuck, what’s concentrating, and what needs intervention.

A practical structure is two views: an operations view (daily/weekly queues: pending confirmations, open exceptions, aging) and a management view (monthly trends: coverage, utilization, concentration, cohort performance).

Add simple action triggers (for example: confirmation delays crossing a threshold, dispute rate drift, stuck items accumulating) so reviews lead to decisions, not debates. When MIS is designed this way, the program can be steered with consistency even as scope expands.

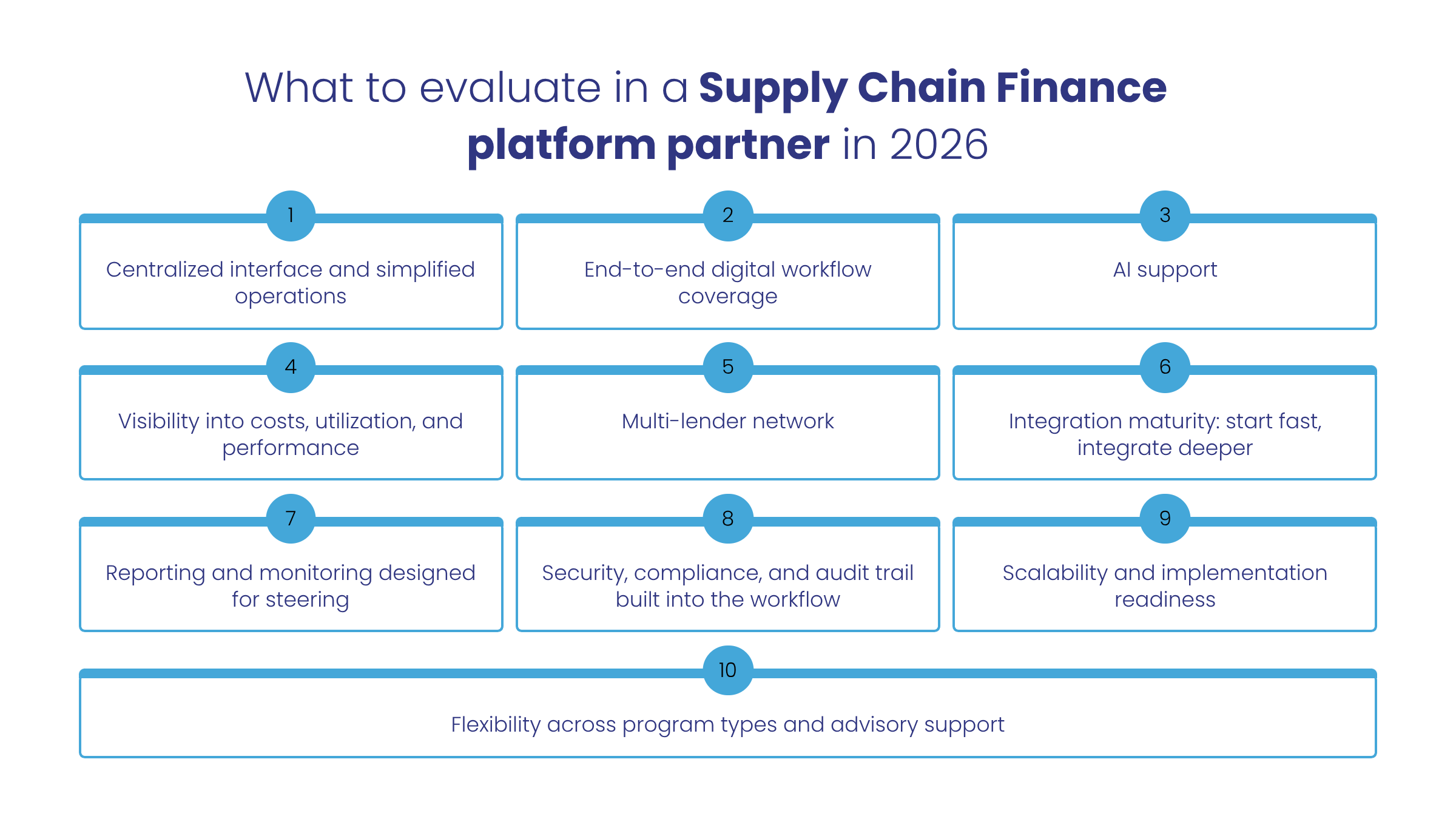

What to evaluate in a Supply Chain Finance platform partner in 2026

A platform partner becomes strategic when it helps you scale coverage without scaling operational effort in the same proportion. In 2026, the best way to evaluate partners is to look beyond headline pricing and ask how the partner will run the program day-to-day—through confirmations, exceptions, visibility, and adoption.

1. Centralized interface and simplified operations

You want one operating view across counterparties, invoices, approvals, and settlement status. The practical benefit is fewer handoffs and fewer parallel versions of truth across procurement, sales ops, and finance. Ask to see how the platform surfaces what’s pending, what’s stuck, and who needs to act—without manual follow-ups.

2. End-to-end digital workflow coverage

Evaluate whether the platform supports the full flow from invoice capture to closure: role-based approvals, evidence capture for confirmations, structured exception queues, and traceable settlement. The goal is predictable throughput, so the program runs on cadence rather than chasing.

3. AI support

AI should show up as operational improvements: earlier anomaly flags, better prioritization of stuck items, faster routing of exceptions to the right owner, and fewer repetitive checks. The test is simple: does it reduce cycle time and exception backlog without adding new complexity for teams?

4. Visibility into costs, utilization, and performance

A corporate program benefits when you can see not only volumes, but also utilization patterns, turnaround times, and performance by cohort. Ask for views that help answer: which partners use the program repeatedly, where cycle times are slipping, and how costs behave across cohorts and program types.

5. Multi-lender depth

This is a key 2026 differentiator. A multi-lender setup reduces dependency on a single funding source and improves continuity when credit appetites shift. It also helps expand coverage across partner segments because not every supplier or distributor fits the same lender profile.

Ask:

- How many lender relationships are active on the program type you need

- How lender-fit is determined for different counterparties/cohorts

- What happens when one lender pauses a segment – can the program continue without redesign?

- Whether reporting can show lender-wise concentration and performance (so risk stays visible)

6. Integration maturity: start fast, integrate deeper

A strong partner won’t force heavy integration to begin, but should be ready to connect as you scale: ERP/accounting connectivity, master data sync, reconciliation support, and secure APIs. Ask for a maturity path: what’s recommended for the pilot, and what changes once volumes grow.

7. Reporting and monitoring designed for steering

Dashboards should support steering decisions: coverage and activation (onboarded vs active), confirmation turnaround, exception health and aging, concentration, utilization trends, and early-warning indicators. Leadership shouldn’t need manual stitching to understand the month.

8. Security, compliance, and audit trail built into the workflow

You should be able to trace why an invoice was eligible, who confirmed it, what happened in exceptions, and how it closed—without searching across emails and spreadsheets. Look for encryption, role-based access, and audit-ready logs as standard.

9. Scalability and implementation readiness

Beyond go-live, assess how expansion is handled: adding new cohorts, managing rule changes, and rolling out new workflows without disrupting operations. Ask for realistic implementation timelines, resourcing expectations, and how onboarding is supported at scale.

10. Flexibility across program types and advisory support

Even when you begin with one program model, most corporates add others over time. A strong partner should support multiple Supply Chain Finance structures within one operating layer and guide you on sequencing so expansion is planned, not reactive.

Conclusion

For Indian corporates, Supply Chain Finance programs create the most value when they stay predictable at scale, not just in a pilot. That predictability comes from a few fundamentals: a clear outcome, deliberate sequencing, a shared “confirmation truth,” disciplined exception handling, and clear reporting without month-end reconstruction.

As you take a 2026 lens to this, it’s worth evaluating whether your current operating layer is set up to expand coverage without expanding follow-ups. The right platform partner should make three things easier at the same time: run multi-lender programs through one interface, keep workflows digital from billing to collection, and help improve penetration by matching borrowers to the most suitable lenders.

Loan Frame is built around that operating requirement: a multi-lender Supply Chain Finance marketplace connected to top Indian banks and NBFCs, with a unified interface and digital workflows. It also brings a practical execution layer: partner activation and onboarding support, invoice handling and MIS, renewal coordination, and structured help on stale invoices and escalations, backed by transparent pricing.

Request a call back to see how we can help with your Supply Chain Finance requirements.