When you sell on credit, you don’t just book revenue, you also lock up cash in invoices that will be paid weeks or months later. Over time, that adds up: strong billing, a solid customer list, and a receivables line that keeps growing faster than your bank balance.

Receivables financing is a way to turn part of that line into usable cash. Approved invoices on anchor corporates, distributors, and dealers become the base for short-tenor funding that follows your actual trade flows. Buyers still pay on their usual terms; you simply access a portion of that cash earlier, in a structured way.

This article explains how that works in practice: what receivables financing is, where it fits in your working capital mix, the main structures available, and how you can use them to make your receivables book behave more like a planned cash-flow stream than a number you only track at month-end.

What Is Receivables Financing?

Receivables financing is short-term funding taken against your approved sales invoices, instead of against a generic working capital limit or collateral.

You use invoices raised on anchor corporates, distributors, or dealers as the base for finance. A financier advances a portion of the invoice value before the due date and is repaid when the buyer pays the invoice. The commercial terms with your customer stay the same; the only change is when you receive part of the cash.

In simple terms, three things happen:

- You deliver and raise an invoice

You supply goods or services, issue an invoice with a clear due date, and have the usual supporting documents in place (PO, contract, delivery proof, e-invoice details where needed). - You get an advance on that invoice

A financier agrees to fund a portion of the invoice value, say 80–90%, based on the buyer and agreed rules. You receive this money before the due date. - The invoice is paid and the funding is settled

When the buyer pays, the financier recovers the advance and charges. Any remaining amount due to you is passed on as per the agreed structure.

Your underlying business doesn’t change:

- You still own the customer relationship.

- Your customer still pays their invoice on the same terms.

What changes is that part of the value in your receivables becomes available as cash, when you actually need it.

“Receivables financing” is a broad label for several ways of doing this, whether it’s funding invoices on large buyers, factoring receivables, or financing receivables on distributors and dealers. All of them work off the same idea: approved invoices as a base for short-term, self-liquidating finance.

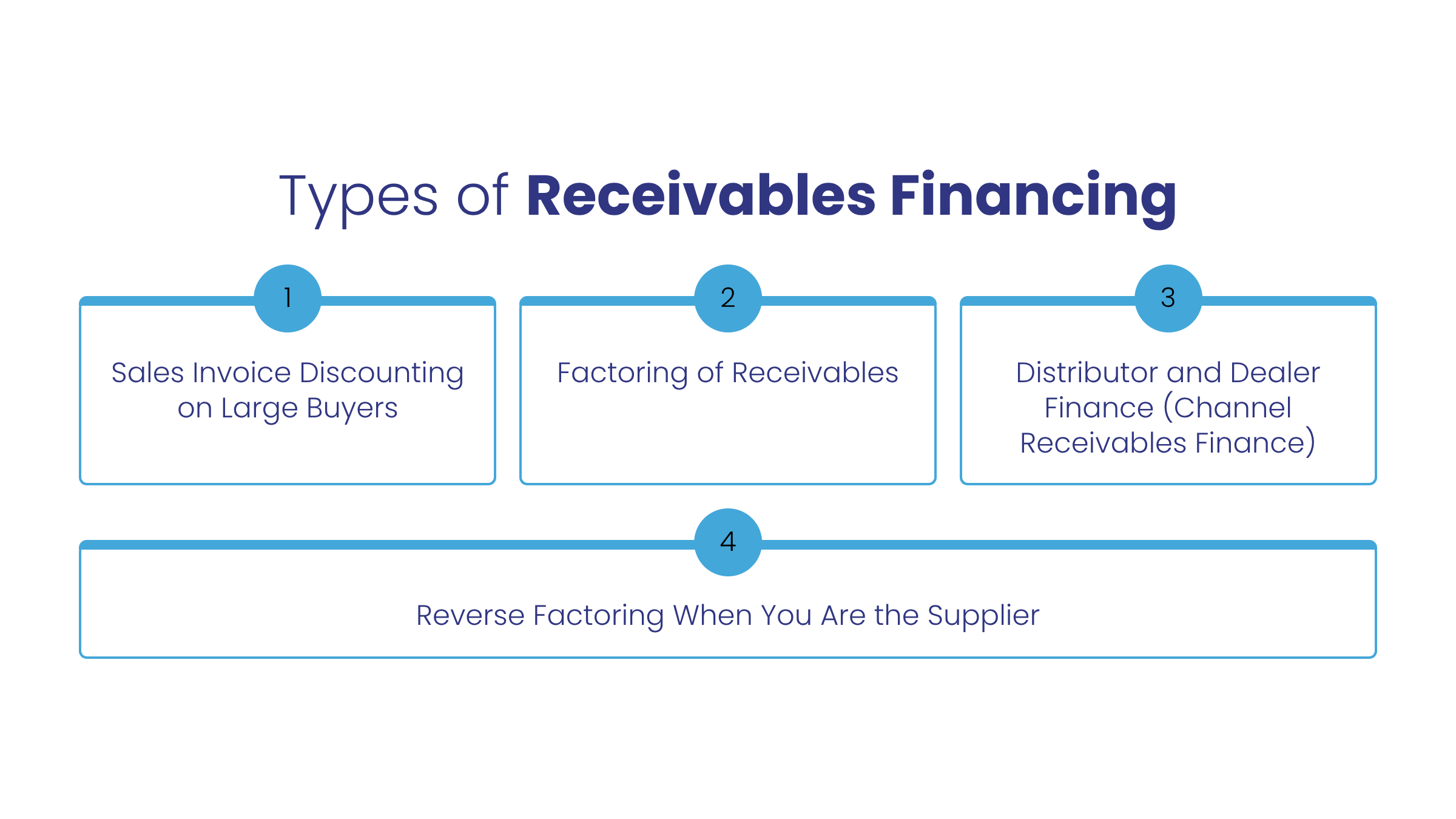

Types of Receivables Financing

1. Sales Invoice Discounting on Large Buyers

Here you fund directly against invoices on large, well-rated buyers: corporates, PSUs, marketplaces, or major retailers.

- You raise and get the invoice approved.

- A financier advances an agreed percentage of the invoice value.

- The buyer pays on the due date and the advance is settled.

You keep control of the relationship and collections, while using the buyer’s strength and your track record to unlock liquidity. This works well where you have concentrated exposure to a few anchors with long terms.

2. Factoring of Receivables

Factoring adds structure around both funding and receivables management.

- You assign a pool of receivables to a factor.

- The factor advances most of the value upfront.

- Collections are routed through the factor, who maintains the ledger and manages recoveries within agreed rules.

3. Distributor and Dealer Finance (Channel Receivables Finance)

Channel finance focuses on your distributor and dealer receivables.

- Dealers purchase from you on credit.

- A financier pays you against approved dealer invoices, often soon after dispatch.

- The dealer repays the financier on extended terms.

From your perspective, the dealer receivable converts to cash on Day 1, and the financier carries the dealer exposure within defined limits. This is effective in sectors with wide networks such as FMCG, durables, IT hardware, industrials, auto and ancillaries, where you want higher stocking and deeper reach without stretching DSO.

4. Reverse Factoring When You Are the Supplier

Reverse factoring is set up by the buyer, but if you are the supplier into a strong anchor, it operates as receivables finance on that anchor.

- The anchor sets up an early-payment programme with one or more financiers.

- You upload invoices; once the anchor approves them, you can opt for early payment from the financier.

- The anchor settles with the financier on the original due date.

You reduce DSO on that buyer and often benefit from pricing linked to the anchor’s credit profile, without having to arrange separate facilities for each relationship.

Why Receivables Financing Matters for Indian Corporates

For most Indian corporates, receivables rise every time you add an anchor, enter a new region, or extend credit to the channel. Revenue grows, but cash takes longer to catch up. Receivables financing helps you manage that gap in four practical ways.

1. Align cash with how you actually sell

Credit terms with large buyers and distributors are usually long. Billing may be strong, but collections land weeks later. Funding a defined share of approved invoices helps you:

- Bring cash closer to the date of sale

- Rely less on end-of-month collection pushes

- Give treasury a clearer view of expected inflows

You move from uncertain “60–90 day” realisation to more predictable cash against a known receivables pool.

2. Support growth without constantly stretching limits

New channels, tenders, launches, and peak seasons all increase dispatches and receivables. Using only traditional lines for this can be limiting. With receivables financing:

- Capacity expands in line with volumes on selected buyers and channels

- Funding stays short-tenor and linked to real trade, not long-term leverage

You can take larger orders or raise dealer limits with a clearer view of how that additional outstanding will be funded.

3. Protect key relationships

Sudden tightening of limits or aggressive collections can damage buyer and dealer relationships. A receivables programme gives you more room to:

- Maintain or selectively improve terms for strategic accounts

- Keep discussions focused on business, not just overdue payments

Financing runs in the background. What your customers and partners experience is reliable supply and consistent credit support.

4. Improve visibility and discipline on receivables

To use receivables financing well, you need clean data on:

- Which invoices are fully approved and dispute-free

- How ageing behaves by buyer, region, and channel

- Where deductions, delays, and claims keep repeating

Setting up a programme forces this clarity. Over time, it usually leads to tighter reconciliations, better credit calls, and a common picture of receivables across finance, treasury, and sales.

The Receivables Financing Process

Different products work slightly differently, but most receivables financing programmes follow the same basic lifecycle. Once you see it end-to-end, it’s easier to design something that fits your set-up.

1. Programme design and portfolio selection

You start by deciding which receivables to finance.

- Choose target segments: large enterprise buyers, specific distributors/dealers

- Set eligibility rules: minimum invoice size, maximum tenor, required documents, ageing limits

- Agree advance rates and pricing bands with participating financiers

This is where treasury, finance, and credit align the programme with existing policies and banking relationships.

2. Connecting invoices and approvals

Next, you need a reliable way to move invoice and approval data into the platform.

- Invoices are generated in your ERP as usual

- Acceptance is captured via buyer confirmation or internal checks on delivery and terms

- A system connection (API, SFTP, or similar) sends approved invoice data and basic documentation to the platform

This reduces manual work and keeps the funding view aligned with your books.

3. Eligibility checks and funding pool creation

Once invoices land on the platform, the agreed rules are applied:

- Is the buyer or dealer in scope?

- Is the invoice within allowed ageing and tenor?

- Are required fields and documents complete and consistent?

- Are buyer-level and overall limits within range?

Eligible invoices move into a funding pool, showing how much can be advanced at any point.

4. Drawdowns

Treasury then decides how and when to draw.

- Funding can be automated for selected buyers and channels, or

- Used tactically around peaks, tenders, or seasonal build-ups

Once you confirm, advances are disbursed to your chosen account and the system records which invoices were funded, when, and on what terms.

5. Collections and settlement

When buyers or dealers pay:

- Funds flow into designated accounts

- Collections are matched back to funded invoices

- The financier recovers principal and charges

- Any reserve or surplus is passed back to you

Delays, short-pays, and disputes are flagged at invoice level and handled under pre-agreed rules.

6. MIS, controls, and adjustments

Throughout the programme you can see:

- Funded vs eligible receivables by segment

- Utilisation by lender and buyer

- Ageing of funded and unfunded invoices

- Exceptions and dispute buckets

This lets you adjust the programme over time – adding or removing segments, tuning advance rates, and resetting limits based on actual performance rather than guesswork.

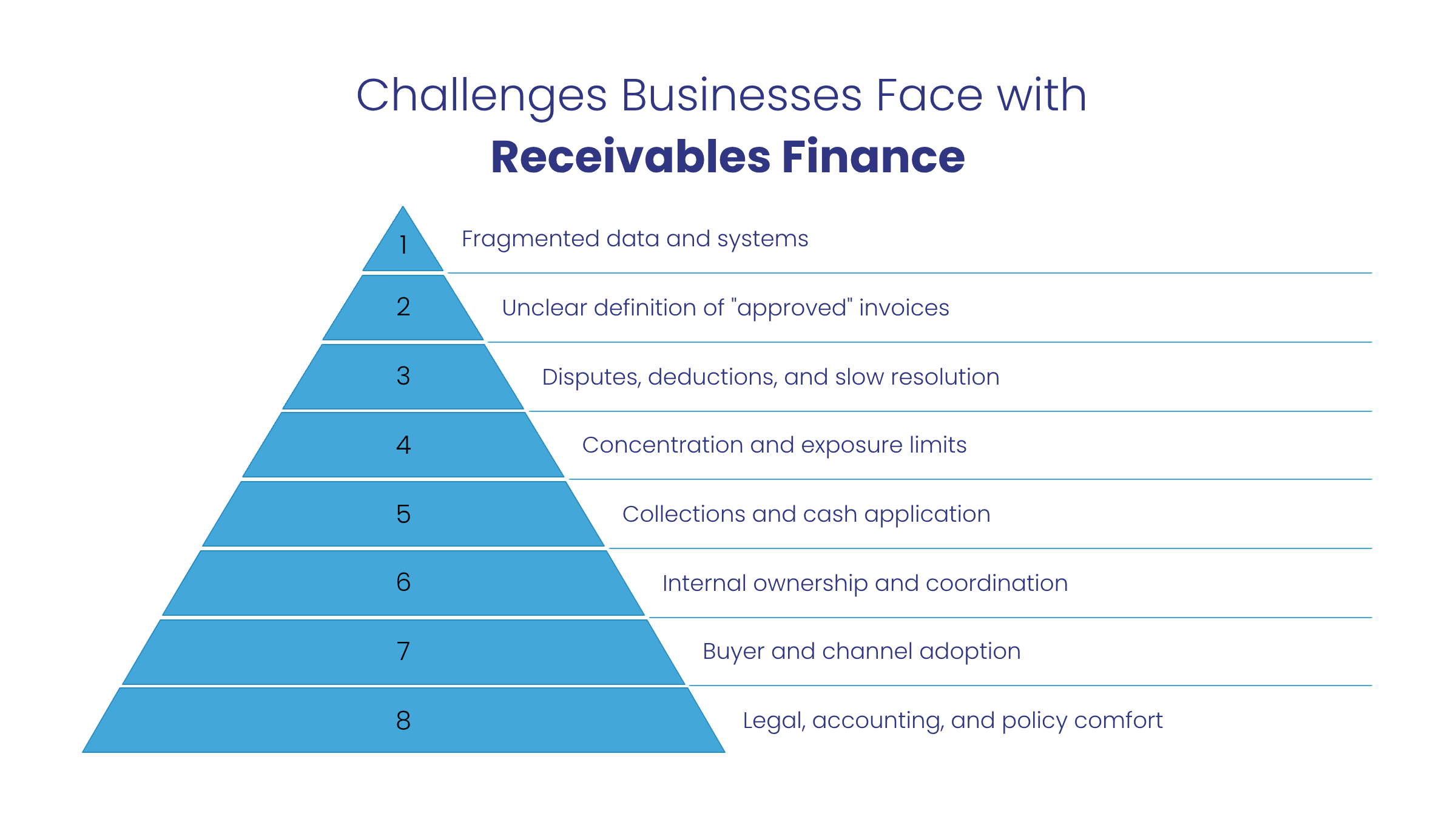

Challenges Businesses Face with Receivables Finance

Receivables financing looks straightforward on paper: clean invoices in, cash out, collections back in. In practice, corporates run into a few common roadblocks that limit scale or make programmes harder to run than they should be.

1. Fragmented data and systems

Receivables data is rarely in one place.

- Multiple ERPs or instances across plants and business units

- Inconsistent customer masters and credit terms

- Invoice details, credit notes, and deductions stored in different systems

When this isn’t standardised, it becomes harder to:

- Prove what is actually “approved” and eligible

- Give financiers confidence in the numbers

- Match collections back to funded invoices cleanly

2. Unclear definition of “approved” invoices

Different teams often mean different things by “approved”:

- Sales considers an invoice valid once it is raised

- Operations looks at delivery

- Finance waits for GRN/PoD, dispute checks, and internal sign-offs

Without a single, agreed definition, you get:

- Invoices pushed for funding before they are truly clean

- Frequent exceptions and reversals

- Lower advance rates or tighter rules from financiers

3. Disputes, deductions, and slow resolution

Price claims, quantity disputes, returns, and promotional deductions are a part of B2B trade. The challenge is when:

- Disputes are logged in emails or spreadsheets

- Credit notes are delayed or not matched to specific invoices

- Short-pays sit unexplained for weeks

Financiers react by tightening eligibility or excluding entire buyer segments, which reduces the usable part of your receivables base.

4. Concentration and exposure limits

Many corporates have:

- A few large anchors driving a big share of receivables

- Channel exposure concentrated in certain regions or dealer clusters

This creates challenges such as:

- Financiers capping exposure on specific buyers or sectors

- Rapid utilisation of limits on a small set of names

- Sensitivity to any slowdown or stress in those pockets

Without conscious concentration management, programme size can hit a ceiling quickly.

5. Collections and cash application

Funding is only half the story; settlement matters just as much. Issues usually show up when:

- Collections from financed and non-financed invoices are mixed in the same account

- Remittance information is incomplete or inconsistent

- Cash is applied at account level, not invoice level

This makes it harder to:

- Reconcile funded positions

- Release reserves quickly

- Maintain confidence in reported ageing and DSO

6. Internal ownership and coordination

Receivables finance touches multiple teams: sales, finance, treasury, credit control, operations. Common friction points:

- No clear “owner” for the programme

- Sales promising things the facility cannot support

- Finance and treasury seeing it only as a reporting or compliance item

Without a single owner and defined roles, programmes tend to stay pilot-scale, and avoidable issues take too long to resolve.

7. Buyer and channel adoption

Even a well-designed programme can stall if buyers, distributors, or dealers don’t engage. Typical reasons:

- Complex explanations of pricing and cash flows

- Extra documentation that feels duplicative

- Early operational glitches that aren’t addressed visibly

If partners don’t see a clear benefit and a simple process, they default to existing ways of working, and utilisation remains low.

8. Legal, accounting, and policy comfort

Finally, internal comfort on structure and treatment matters:

- How facilities sit relative to existing covenants and security

- Whether arrangements are with or without recourse, and how that’s documented

- How funded receivables are shown in the financial statements

If these questions are not resolved upfront with finance, legal, audit, and risk aligned, approvals slow down and programme design may need multiple iterations.

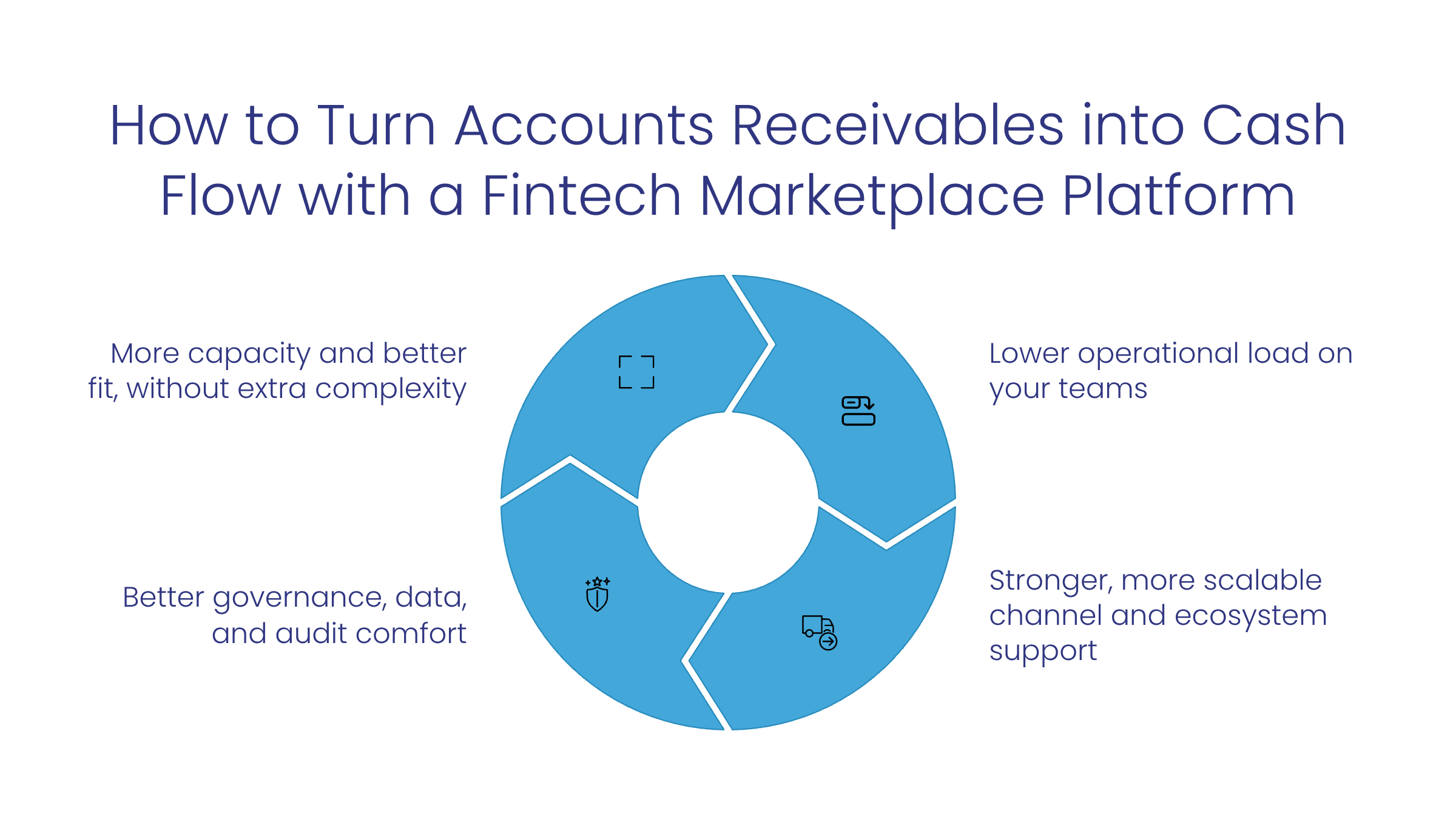

How to Turn Accounts Receivables into Cash Flow with a Fintech Marketplace Platform

You can run receivables programmes separately with individual lenders. A fintech marketplace platform lets you do the same things at a different scale without multiplying effort.

1. More capacity and better fit, without extra complexity

A marketplace connects your receivables to multiple banks and NBFCs through one operating layer.

- Different lenders can take different slices of your book such as large buyers, mid-market customers, dealers.

- You don’t need separate processes and integrations for each lender.

- Dependence on any one counterparty reduces, while overall capacity on receivables improves.

You get more and better-matched limits on the same receivables base, instead of building multiple programmes from scratch.

2. Lower operational load on your teams

The numbers only work if the day-to-day effort is manageable. A marketplace platform can:

- Handle digital onboarding for distributors, dealers, and suppliers.

- Automate invoice ingestion, eligibility checks, and basic document review.

- Enable straight-through drawdowns and standardised settlement flows.

Your teams spend time setting rules, monitoring performance, and handling real exceptions, not compiling files and reconciling scattered statements.

3. Stronger, more scalable channel and ecosystem support

Once financing touches the channel, execution becomes part of your promise to partners. A marketplace model helps you:

- Offer consistent finance options to a broad set of dealers and distributors on one infrastructure.

- Align limits and tenors with actual order patterns, seasons, and product cycles.

- Keep the experience simple for partners, even when several lenders are involved in the background.

For your ecosystem, it feels like a natural extension of their relationship with you, not a separate banking journey they have to figure out.

4. Better governance, data, and audit comfort

Programmes are easier to defend in committees and audits when everything is visible in one place. A good platform provides:

- A single view of funded vs eligible receivables, limit usage, and ageing.

- Clear trails from invoice upload to final settlement.

- Data to compare cost, utilisation, and performance across segments and products.

Receivables financing then sits as a visible, governed part of your working capital strategy, not a collection of one-off lines scattered across lenders and business units.

Conclusion: Putting Your Receivables to Work

Receivables are not going away. You will always have anchors on long terms, distributors and dealers on credit, and suppliers who need predictable payments. The question is whether this remains a passive consequence of growth, or whether you treat receivables as a planned, well-governed funding layer that supports large buyers and the channel without adding balance-sheet strain.

A good receivables financing setup does three things at once: it links directly to your billing and approval flows, gives multiple lenders controlled access to different parts of your book, and runs on consistent rules for eligibility, limits, and collections. That is what turns invoice-level funding from a one-off arrangement into part of your working capital architecture.

Loan Frame is built for that use case. It is a multi-lender supply chain finance marketplace that connects your corporate, supplier, and channel receivables to top Indian banks and NBFCs through a single platform.

The platform layer handles the operational detail that usually slows programmes down: digital onboarding of suppliers, vendors, distributors, and dealers; automated invoice ingestion and rule checks; seamless ERP integration; and real-time MIS on funded vs eligible receivables, ageing, and utilisation for all stakeholders. Around this, Loan Frame’s team runs the day-to-day engine corporates actually need: programme design, ecosystem onboarding support, coordination with lenders, stale-invoice and exception handling, so finance, treasury, and sales see one coherent view instead of fragmented lines.

Book a demo to see what this could look like on your own receivables book across large buyers, suppliers, and the channel.